The Business Case for Direct Air Capture

Critics would argue that it is difficult to make a business case for Direct Air Capture (DAC).

DAC is still in its early stages. It’s a technology that works well even at this early stage of development, and very much like solar and wind power in their infancy, it would be unreasonable to expect DAC to reach maturity without allowing time for investment in continuous innovation.

With the right mix of policy support, tech development and commercial interest, the case for DAC is compelling, especially considering the scale of the climate crisis and the limits to what emissions reduction alone can achieve.

DAC Costs are Falling

As DAC technology is advancing, costs are tumbling to around €300 to €600 per tonne CO₂ captured, down from over €1,000 per tonne in early iterations. That’s no small drop.

More promising still, some emerging systems are showing potential to come in around €100 – €200 per tonne, especially if low grade waste heat is used.

These cost reductions stem largely from improvements in sorbent technology and better heat and energy integration. With each new pilot or demonstration plant, engineers gain insights that lead to cost efficiencies and technical refinement.

It’s worth remembering that this pattern of progress mirrors what we’ve seen before in clean technology. The cost of solar panels, for example, has dropped more than 90% in the past two decades. That wasn’t due to any single breakthrough, but rather an accumulation of incremental gains: more efficient manufacturing, economies of scale, and consistent policy backing.

Driving Down the Cost of DAC Technology

Advantages of DAC for Carbon Removal

DAC systems can be located anywhere and use off-grid, renewable energy sources. This location flexibility also makes it a candidate to deal with hard-to-abate emitters like the aviation industry. (For more, see: Advantages of Direct Air Capture)

What Measures will Drive Down the Cost of DAC?

Cost Reductions Through Scale

As more units are deployed, costs come down. Estimates from the IEA suggest that with proper scaling, DAC costs can fall to $100–$300 per tonne within the next decade.

Waste Heat Input

By co-locating DAC units with, for example, hydrogen electrolysers or data centres, the energy costs are greatly reduced as the low grade waste heat emitted from these processes can be used by the DAC system. To illustrate this, by using waste heat input NEG8 Carbon’s DAC unit’s energy consumption is reduced by about 70%.

See: Direct Air Capture + Waste Heat Use Cases

Modular Design

DAC can be deployed rapidly. Unlike many large infrastructure projects, DAC plants can scale from small to very large depending on location and usage. This allows for rapid iteration and mass production, further pushing down costs.

Long-Term Offtake Agreements

Corporations like Microsoft, Stripe and Google are signing multi-year deals to purchase CO₂ removals and permanent storage from DAC developers. These contracts create predictable revenue streams, helping secure finance and encouraging further development.

Access to Cheap Renewable/Low Carbon Energy

Whether it’s geothermal in Iceland or solar in desert regions, low-cost clean power is essential. Co-locating DAC plants with abundant green energy sources, includign nuclear, is one way to keep operating costs manageable.

CO₂ Infrastructure Buildout

Captured carbon has to go somewhere. It can be sequestered in deep saline aquifers or depleted oil/gas wells, used in materials like concrete, or piped to central storage locations using a network of pipelines. The sooner this infrastructure is built, the faster DAC can scale.

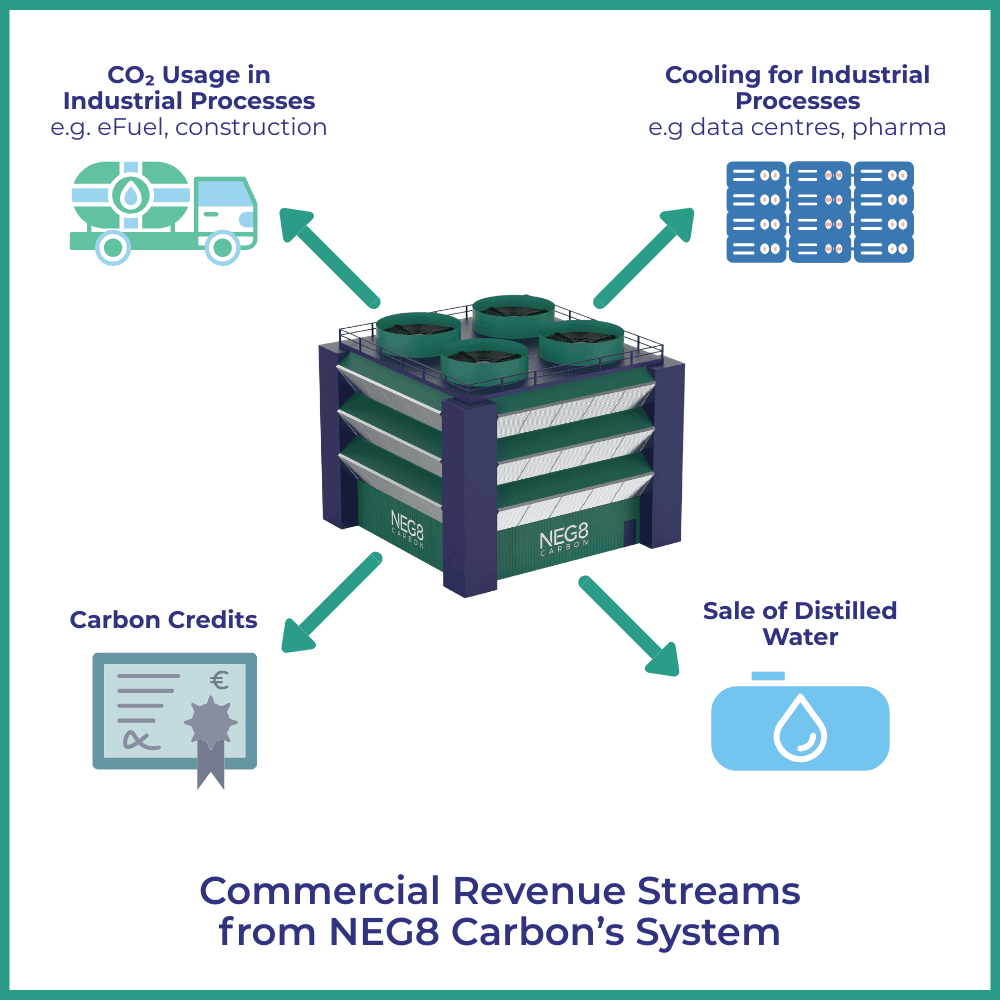

Additionality and Co-Benefits in the Business Case for DAC

What really strengthens the business case for DAC, however, is its potential for additional value streams.

Instead of just storing carbon, DAC can enable the creation of new products and services or be used in existing processes. These include eFuels, construction materials, chemical feedstock, and in food and beverages.

Take these examples:

- Producing cement-free concrete using industrial by-products and captured CO₂. (CarbiCrete)

- Using captured CO₂ for use in greenhouses. (SkyTree)

- Sparkling beverages and beer can make use of captured CO₂. (Aircapture & Almanac Beer | Climeworks & Coco-Cola)

These cases illustrate how DAC can serve as a feedstock supplier, not just a sink. In the near term, before large-scale sequestration networks are fully operational, this kind of CO₂ utilisation could make the difference between a viable DAC plant and one that never gets built.

For more, have a look at these DAC use cases:

- eFuel

- eMethanol

- Sustainable Aviation Fuel (eSAF)

- Methanol-to-Jet Fuel

- Sustainable Data Centres with Direct Air Capture

- Decarbonising Construction by Storing CO2 in Concrete

- Industrial Decarbonisation with Direct Air Capture

The Outlook for Direct Air Capture Over the Next 5-10 Years

Looking ahead, the next decade will be important for DAC. First-generation firms may struggle with scale as early technical limitations hinder progress. However, second- and third-generation companies, those with more efficient systems, better cost structures, and stronger investor backing, will likely come to the fore.

We can expect to see:

More Demonstration Plants

Facilities capturing from 1,000 tonnes per year and more will begin operation, proving feasibility and drawing further investment.

Mergers and Acquisitions

Larger firms may acquire DAC innovators to secure IP or manufacturing capabilities.

Standardisation and Certification

Improved monitoring and verification frameworks will help build trust in DAC credits, allowing them to be traded more widely.

Geographic Hubs

DAC facilities will cluster near renewable energy and geological storage sites.

Blended Finance Models

Public-private initiatives will become more common, helping de-risk early projects.

Market Differentiation

As carbon markets mature, removals using DAC will command higher prices than nature-based offsets, due to their durability and measurability.

The IEA believes that by 2030, DAC needs to be removing 85 million tonnes of CO₂ per year and 980 million tonnes per year by 2050. That’s still only a portion of what’s needed overall in total carbon removal which is over 10 billion tonnes per year.

Carbon Credit/Offset Markets Growth

The carbon markets are said to be heading for a steep growth period with the combined value of carbon credits and voluntary offsets reaching into the trillions of dollars by 2050 (report by Wood Mackenzie, 23 June 2025). This is due to tighter regulations, stricter rules on offset quality, and carbon capture tech development. Furthermore, the CCUS market would need to grow to 4-6 GtCO₂ per annum by 2040-2050 to meet net-zero targets. (McKinsey)

The Role of Policy and Regulation

Market forces alone won’t drive DAC deployment at the scale required. Companies are unlikely to purchase large volumes of carbon credits unless required to do so, or unless those credits hold strong economic or reputational value. This is where regulation plays an important role.

Fortunately, we’re starting to see movement. For example, the European Union’s Emissions Trading System (ETS) is evolving to include high-durability carbon removals. And Japan’s GX (Green Transformation) Emissions Trading System (GX-ETS) is a core policy in the country’s plan to achieve carbon neutrality by 2050. Initially launched in April 2023 as a voluntary, baseline-and-credit system, it will transition to a mandatory system from 2026.

While in the United States, the Inflation Reduction Act provides a generous $180 per tonne tax credit for DAC under the 45Q programme. Such incentives change the maths for investors, reducing risk and making early-stage projects more bankable, although there is a political tug-of-war around these incentives at the moment.

Government Support

Governments have a broader role to play, too. Upfront capital expenditure is required for DAC and without state support or public-private finance mechanisms, many promising DAC ventures will struggle to scale.

But the cost of inaction measured in extreme weather, crop loss, health impacts and infrastructure damage is likely to be far higher. Investing in DAC now could save billions down the line. (See: Direct Air Capture Cost Compared to Cost of Inaction on Climate Change)

There are encouraging examples of governments taking pro-active steps: the UK government announced in October 2024 that it had made available £21.7 billion in funding for CCUS projects in the UK, and the Danish government has made available €1.1 billion in a scheme to roll-out CCUS technologies.

Final Thoughts: Why DAC Matters

The truth is, even if we stopped all fossil fuel emissions today, we’d still have the problem of the excess CO₂ already in the atmosphere which is an estimated 1 trillion tonnes. To try to bring the CO₂ level back to the ~350 ppm of 1990 we would need to remove 500 billion tonnes at least.

Reducing emissions alone can’t fix that. We need removal strategies, and DAC is one of the only approaches that offers scale, permanence, and verifiability. (For more, see: Why Direct Air Capture)

Looking 25 years into the future, one can imagine a world where DAC is no longer seen as a novel technology, but as a normal part of how we maintain climate stability. To get there, though, we must act now. The window to scale DAC in time is narrow, but the opportunity is enormous.

In the end, with the right blend of policy, innovation and support, DAC can emerge from a niche experiment into one of our most powerful tools for repairing the climate.

For more:

- What is the Value of a Carbon Credit?

- Cost of Carbon Capture – How NEG8 Carbon is Making DAC Economically Viable

- Gastech 2025: Building a Robust Foundation for Direct Air Capture Market Growth