Carbon Emissions Reduction with DAC: Three Scenarios

3 October 2025

By: Ray Naughton, Founder & Managing Director of NEG8 Carbon

Direct Air Capture (DAC) technology sits at the intersection of climate action and industrial opportunity. Its path over the next 25 years could go through three possible scenarios, from pragmatic business adoption today to a future of climate-driven urgency.

Scenario 1: The Business Case Period

In the early years of DAC, storage options for captured carbon remain limited. As a result, the emphasis falls on additionality, the tangible benefits that come from using CO₂ in productive ways. Companies adopting DAC at this stage can gain both reputational and financial rewards.

At this point, governments should take up the mandate to help fund early stage DAC development and back ventures that make a viable business case for DAC-plus, for example, in these DAC + waste heat examples.

In order to make DAC viable, it needs to be economically attractive to investors and project developers. There is a solid business case emerging for DAC, with positive factors such as: the cost of DAC is falling as technology matures, and regulations, policies and stricter penalties are putting pressure on governments and industries to drive towards net-zero.

Additionality

Additionality and coupling DAC with other processes makes DAC a more attractive proposition by making it financially feasible.

DAC supports a range of CO₂ utilisation pathways that can create economic value while contributing to decarbonisation. Examples –

Captured CO₂ can be used in synthetic fuels, particularly e‑fuels and Sustainable Aviation Fuel (SAF), where it is combined with green hydrogen to produce hydrocarbons via processes like Fischer‑Tropsch synthesis. This approach provides a route to low‑carbon fuels for hard‑to‑decarbonise sectors such as aviation and shipping.

DAC‑captured CO₂ can also feed into building materials, such as concrete, aggregates, or carbon‑cured cement, where it is mineralised to provide long‑lasting carbon storage.

Other applications (see: What is CO₂ Utilization) include usage in food and beverages, chemical feedstocks (e.g. urea), dry ice, in greenhouses, CO₂ batteries, and plastics production. While these shorter‑lived uses eventually release CO₂ back into the atmosphere, they can displace fossil‑derived CO₂ and support the early commercialisation of DAC technology by generating revenue streams.

In short, government incentives combined with practical industrial uses make a convincing case for DAC deployment during this period.

Scenario 2: Guarding Against Climate Escalation

As DAC technologies mature and costs fall, attention shifts towards permanent or long-term storage of CO₂. This includes injecting captured carbon into depleted oil and gas reservoirs. These sites already provide proven geological traps and extensive monitoring data.

This scenario depends on strong collaboration between industry and government. Together, they must act to stabilise atmospheric CO₂ levels and prevent escalation to the next stage. The objective is clear: avoid a point where climate panic forces emergency measures.

Scenario 3: A Crisis-Driven Scramble

Looking 25 years ahead, the picture may be dire (although we hope not). Should mitigation efforts falter, the world may find itself in a climate-crisis scramble. In this future, DAC is no longer an option but an obligation, with governments and industries racing to deploy the technology at vast scale.

At this point, every available zero-carbon solution, be it DAC, renewables, hydrogen, storage… would be deployed simultaneously in a bid to reverse or stabilise runaway climate impacts. The urgency would drive rapid build-out, but under conditions of desperation rather than careful planning.

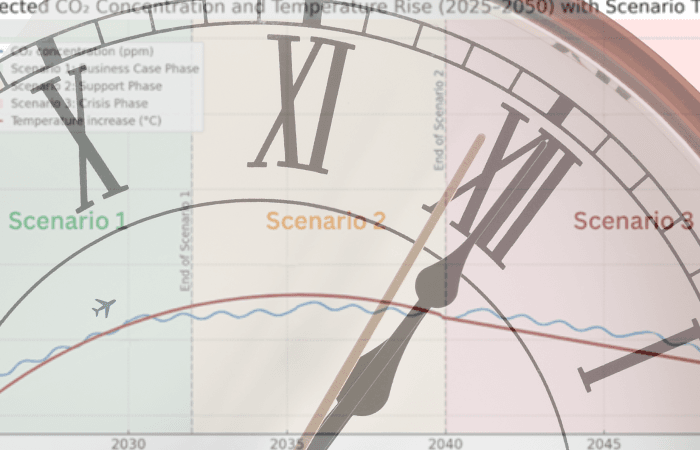

The Next 25 Years: Costs, Concentrations, and Choices

Current atmospheric CO₂ is increasing at an average of ~4 parts per million (ppm) per year. If this continues, average global temperatures are expected to rise by roughly 1°C within 25 years. Data tracking CO₂ concentrations, and corresponding temperature rises, highlight this urgency. The graph below illustatres this point.

The outlook, however, is not without hope. The cost of capturing a tonne of CO₂ is projected to fall steadily as carbon capture technologies scale, while innovation and supportive policies drive progress. Early action, focusing on both business cases and long-term storage, could keep DAC on the path of preparedness, avoiding the costly desperation of Scenario 3.

The following graphs show two possible outcomes. The first is if there are no real carbon capture interventions or significant emissions reduction, and the second shows how CDR efforts can make an impact.

Outlook With No Significant CDR and Emissions Reduction

Outlook With Significant CDR and Emissions Reduction

Conclusion

The story of DAC could unfold in three ways:

- A period of early adoption driven by additional business benefits and government support.

- A stabilisation phase where storage and cooperation hold the line.

- A last-minute scramble to respond to a climate crisis.

The outcome depends on choices made now. By acting early, governments and industries can secure DAC’s role as a planned solution rather than a desperate necessity.

For more:

- Costing Direct Air Capture Deployment Towards Zero and Negative Carbon Emissions

- EU Climate Regulations Explained